50/30/20 Rule Explained: How to Budget Like a Pro

In this article

Money is often a sensitive topic and for many Filipinos, it’s also a major source of stress. According to a study by insurance firm AIA, 59% of Filipinos, or nearly six in ten, worry about money on a regular basis. With rising costs of living and wages that remain largely stagnant, it’s no surprise that financial concerns weigh heavily on most households.

Constant worrying can take a toll on both your mental and physical health. In some cases, this stress can even lead to medical expenses, adding further strain to an already tight budget.

Before things reach that point, it’s important to take small, practical steps toward becoming more financially prepared. Here are simple, budget-friendly tips that can help you worry less about money and regain control over your financial life:

The saying “out of sight, out of mind” may bring peace in some areas of life, but it definitely does not apply to personal finances. If you want to worry less about money, the first and most important step is to track your spending. Knowing where every peso goes helps you avoid overspending and makes it easier to differentiate needs, wants, and luxuries.

I highly recommend using a spreadsheet or budgeting app to list your fixed expenses, savings, and other spending categories. Seeing the numbers clearly helps you make informed decisions and spot areas where you can save.

To stay disciplined, you can even set aside exact amounts for bills or daily spending on your digital wallet or features like SkyroPondo, which helps you separate funds for different financial goals. This simple habit alone can improve your money management significantly.

When researching budget-friendly tips, one of the most popular methods you’ll come across is the 50/30/20 rule:

It’s simple, effective, and easy to follow.

However, it’s not the only budgeting system available, and it may not work for everyone. Some may still prefer the envelope method (sobre system) where you categorize expenses into physical or digital envelopes and allocate a specific amount per category.

This is one of the most practical budgeting methods, especially if you pay in cash or struggle with impulse buying.

The goal is not to follow a very strict structure, but to find a budget system that fits your lifestyle. Once you do, focus on consistency. A budget only works if you stick to it.

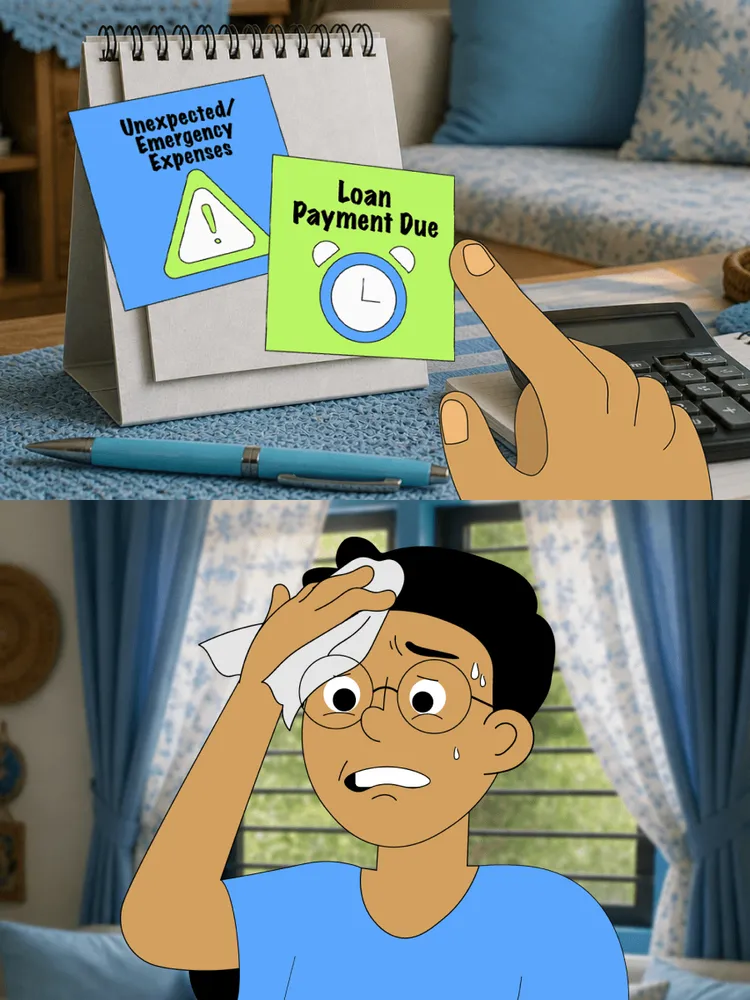

“If I already have savings, why do I still need an emergency fund?”

The answer is simple: your savings are for goals; your emergency fund is for survival.

An emergency fund acts as a financial buffer when unexpected events occur such as job loss, medical emergencies, or urgent home repairs. This is especially important for Filipinos working in remote or freelance roles, where stability can be uncertain. As an independent contractor, a client can end your contract anytime, often without severance pay.

Ideally, aim for 3–6 months’ worth of your salary, enough to cover essentials while you look for replacement income. But with today’s competitive job market, many financial experts now recommend up to 12 months of expenses for added security.

To make your emergency fund work harder, store it in a high-yield digital savings account. You earn interest while keeping the money accessible in case of real emergencies.

Saving money doesn’t mean sacrificing joy; it simply means making smarter daily choices.

If you work onsite, one of the easiest ways to cut expenses is to bring your own packed lunch. A homemade meal can cost half (or even less) of what you’d spend eating out. Coffee drinkers can also save significantly by choosing convenience-store brews instead of premium café drinks.

These small adjustments add up over time. You just need to pick cost-saving habits that still allow you to enjoy life.

While it can take years to earn promotions or salary increases, you don’t need to wait that long to improve your financial situation. One of the smartest budget-friendly tips is to explore side hustles.

If you have marketable skills, consider offering services such as:

As a writer and digital marketer, freelancing helps me supplement my income by offering content services to businesses that need help but may not be ready to hire full-time staff.

If you need tools, equipment, or materials to start a side hustle, you can use SkyroCredit which helps you purchase what you need to grow your income responsibly.

And don’t forget the long-term strategy: upskilling. Learning new skills can open doors to better-paying opportunities. You can study through free platforms like YouTube or invest in structured courses for deeper learning.

Building your savings consistently is already a major step toward financial stability. But even with a solid savings habit, there are times when it’s smarter and more practical to choose flexible installment options, especially when you need to purchase essential, high-ticket items for your home, work, or business.

Instead of draining your emergency fund or long-term savings, you can worry less about money and take advantage of Skyro’s Product Loan, which offers affordable installments for appliances, gadgets, furniture, and other important purchases. It’s a responsible way to manage cash flow while still getting what you need.

Did this help?

See all articles

4.7

46.7K reviews on Google Play

Get approved, track your loan, and pay.