50/30/20 Rule Explained: How to Budget Like a Pro

In this article

Applying for a loan application, whether with Skyro or with another lender, is often a practical step when you need to make an important purchase or need help managing your finances. That’s why it can feel discouraging or confusing when your loan application is denied, especially if you believed you met all the basic requirements.

However, lenders look at several criteria before approving a loan, and even small gaps can affect the outcome. To help you understand what may have happened, keep reading to explore the most common reasons a loan application may be denied and what they mean for you.

📌 Note: Banks, financial institutions, and digital lenders like Skyro do not provide the exact reason for rejection — but the most common factors are listed below.

However, there are several common factors that could have influenced the decision. If your loan application was not approved, you may have experienced one or more of the following situations:

Your credit history is one of the most important factors lenders consider when reviewing a loan application. It helps financial institutions understand how you manage borrowed money. Your credit score is influenced by several elements, including:

If you have a record of late payments, unpaid loans, or accounts sent to collections, lenders may see you as a high-risk borrower. On the other hand, if you have no credit history at all, lenders may also hesitate because they don’t have enough information to check your financial behavior.

A higher credit score doesn’t guarantee approval, but it greatly increases your chances, as it shows responsible borrowing and repayment habits.

Having a source of income is important, but it’s not the only factor lenders look at. When evaluating a loan application, lenders also look at:

Even with a good credit score, a low income may signal that you could struggle with loan payments. Lenders typically want to see that you earn enough to comfortably cover existing expenses and the new loan installment.

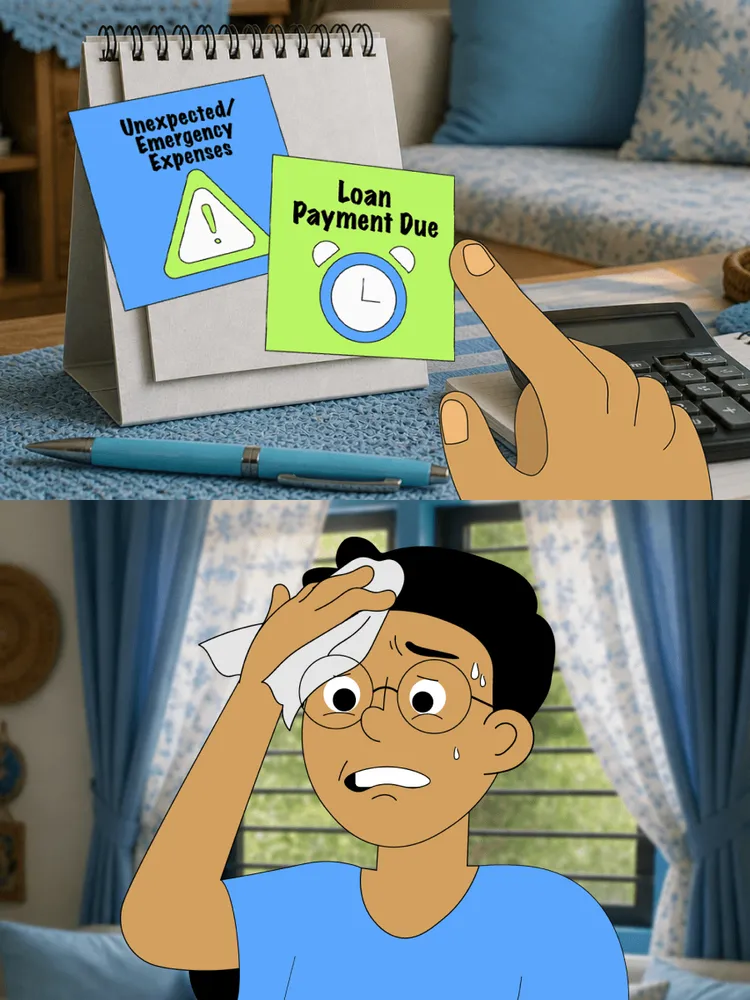

Your debt-to-income (DTI) ratio compares how much you owe each month to how much you earn. This includes expenses such as:

If your existing financial duties already take up a significant portion of your monthly income, lenders may decide that approving a new loan application would put you at risk of not being able to repay it.

Even small documentation mistakes can lead to a rejected loan application. At Skyro, applying for a Product Loan is simple. We only require applicants to:

However, some applicants may:

Other lenders or loan companies may have more complex requirements, such as pay slips, proof of billing, bank statements, or employment documents. Always double-check that all information is accurate and complete before submitting your loan application to avoid unnecessary delays or rejection.

Even a few late payments can negatively affect the outcome of your loan application. Consistently paying bills or existing loans after the due date suggests that you may have difficulty managing repayment schedules.

Lenders want to see a pattern of timely payments, as this indicates responsible financial management. If late payments appear on your credit record, consider improving your repayment habits first before reapplying for another loan.

Sometimes, the issue isn’t your financial history — it’s the loan amount requested. If the amount is too large compared to your income, existing debts, or credit profile, lenders may see it as a higher risk.

Requesting a more realistic and manageable amount increases your chance of approval. As your credit improves and you establish a stronger payment record, you may qualify for higher loan limits in the future.

If your loan application was denied, this doesn’t mean you won’t be able to borrow in the future. It simply means there are areas you can improve before applying again. Take time to review your financial situation and consider the following steps to strengthen your next loan application:

Your credit score plays a major role in loan approval, so building a strong one is worth the effort. Here are a few ways to improve:

If you’re just starting to build your financial profile, consider beginning with credit-building products, such as a small credit line or a basic credit card. These help establish positive repayment history and gradually increase your credit score over time.

A high amount of debt compared to your income can make lenders hesitant to approve a new loan application. To improve your chances:

Lowering your debt-to-income (DTI) ratio shows lenders that you have room in your budget to handle new repayments responsibly.

If low income affects your loan application, adding more sources of earnings may help. Consider:

Stable earnings and a stronger income profile help lenders feel more confident that you can manage loan repayments.

Some lenders offer secured loans that allow you to use an asset, such as a vehicle, equipment, or other property, as collateral. Offering collateral:

However, always make sure you understand the risks before using these as sets as collaterals.

A denied loan application isn’t the end of the road. Once you’ve taken steps to improve your financial standing, you can confidently try again.

When you feel more financially ready, visit our Skyro Product Loan page and explore a wide range of appliances, gadgets, and other essentials available through Skyro. With flexible terms and a simple application process, you can get the upgrade you need and enjoy a smoother borrowing experience moving forward.

Did this help?

See all articles

4.7

46.7K reviews on Google Play

Get approved, track your loan, and pay.