Loan-to-Cash Conversion Schemes: Why They Put Borrowers at Risk

In this article

Looking to budget your finances better, boss? This helps you understand where your money goes every month. With groceries to buy, bills to pay, and savings to build, having a clear budget can help you make the most of your income and stay in control of your finances.

In this guide, we’ll teach you how the 50/30/20 rule works, what to include in each category, and simple budgeting tips for everyday expenses.

The 50/30/20 rule is a simple and popular budgeting strategy to help you manage your finances better. Once you receive your income, here’s the recommended way to divide it:

This budgeting framework was developed by U.S. Senator Elizabeth Warren and her daughter, Amelia Warren Tyagi, and introduced in their book All Your Worth. It offers a practical way to balance your everyday expenses while setting aside money for savings and future financial goals.

When you receive your income, whether it's from your salary, a part-time job, an allowance, or another source, make sure to use only the exact amount that gets deposited into your account.

For example, if your gross salary is ₱30,000, there may still be deductions for taxes and mandatory contributions such as SSS, PhilHealth, and Pag-IBIG. This means your net income might be around ₱26,542.45.

Your ₱26,542.45 is the amount you should use when dividing your budget using the 50/30/20 rule, boss. Based on this amount, your budget would look like this:

50% for needs: ₱13,271.23

30% for wants: ₱7,962.74

20% for savings: ₱5,308.48

Needs are the essential expenses you need to pay for your daily life. These should take up the biggest portion of your income. This commonly includes:

When listing down your needs, ask yourself: “Can I get through the next month without paying for this?” If the answer is no, then it’s likely part of this category. As these are essential expenses, make sure to cover them first before moving on to your other priorities.

For many Filipinos, supporting the family also takes up a big part of the budget. Whether that means contributing to household expenses, helping out with your siblings’ tuition or allowance, remember to include these in your monthly budget.

Wants are purchases that make life more enjoyable but are not essential for everyday living. While they're nice to have, you can always spend less on them when needed. If your budget is tighter this month, these are usually the first expenses you can cut back on or adjust. This may include:

The wants category doesn’t mean giving up the things you enjoy. Your hard work deserves to be rewarded, too. To manage your budget effectively, set a monthly spending limit that still leaves enough room for future plans and financial goals.

Savings is the money dedicated to your future. Whether you’re building your savings, creating an emergency fund, planning for a big purchase or trip, paying off your loan faster, or investing, this part of your budget is essential. This may include:

Remember, boss. Your savings shouldn’t be an afterthought. Once you’ve received your take-home pay or allowance, make sure to set aside the amount for your savings. Small contributions can add up to a lot over time as long as you stay consistent with saving.

While 20% is the recommended amount, it's important to remember that everyone's financial situation is different. What works for others may not always work for you. If saving 20% isn't possible right now, that's okay. Start with an amount that fits your budget, then increase it little by little as your finances improve. Every step toward saving counts, boss!

Now that you know how the 50/30/20 method works, here are some budgeting tips to keep in mind:

If you haven’t made it a habit to track your spending, now is the best time to do so. For the 50/30/20 rule to work, you must always be mindful of where your money is going. This gives you an idea of your spending habits so you can make any changes.

💡 Tip: Use a budgeting app, spreadsheet, or notebook to record your income and expenses

As bills are part of the 50% portion of your monthly income, make sure to pay your bills on time. This helps you avoid extra charges like late fees and interest.

💡 Tip: Keep track of your payment due dates by adding it to your reminders or calendar

Before buying any item, think about why you need it in the first place. Is it a want or a need? You can also wait at least 1-2 days before making a decision. This helps you avoid impulse buying.

💡 Tip: Take a photo or screenshot of the item and save it to your phone’s gallery. If you still want it after a day or two, it may be worth buying

Save before you spend. As the saying goes, “out of sight, out of mind.” It's best to keep your savings in a separate account from the one you use for your bills and everyday expenses. This makes it less tempting to transfer money from your savings when your budget for the other categories is tight. Remember, your savings is meant to help you prepare for the future, boss!

💡 Tip: Open a digital savings account and make it a habit to transfer your 20% savings as soon as you receive your income

The 30% for wants is only meant to serve as a guide. If it doesn’t align with your budget plans for the month, that’s okay. Feel free to customize your spending limit to an amount that’s realistic for you, while still making sure you’re able to set aside money for your needs and savings. Regardless of the amount, the most important thing is to stay consistent.

💡 Tip: Check your spending at the end of each month and adjust your spending limit based on your current income, expenses, and priorities

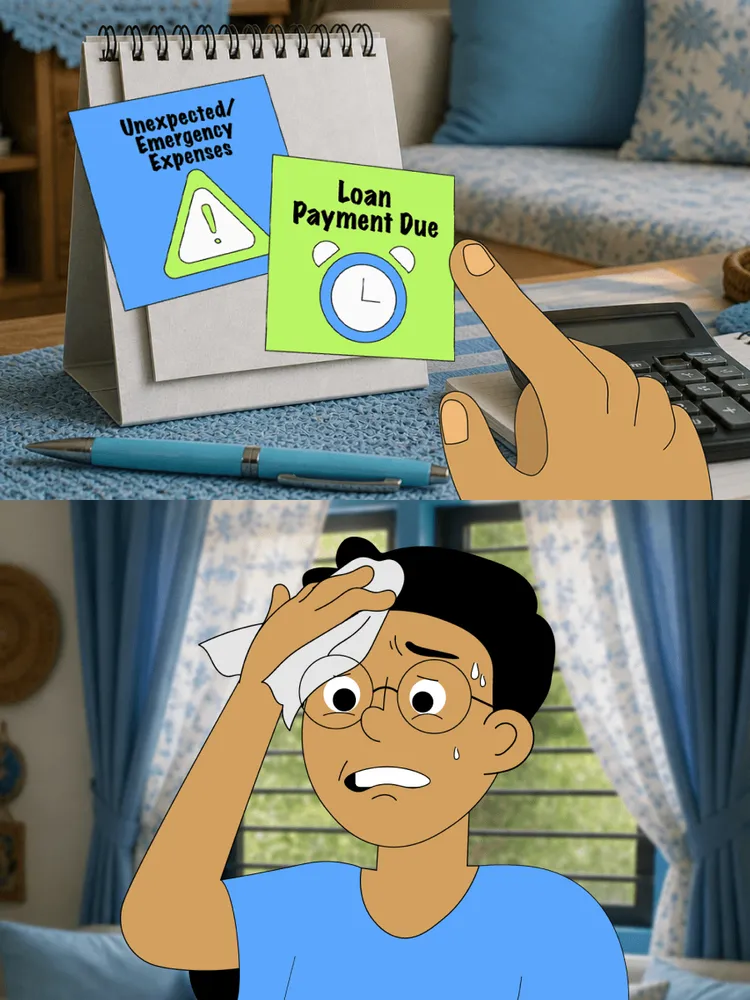

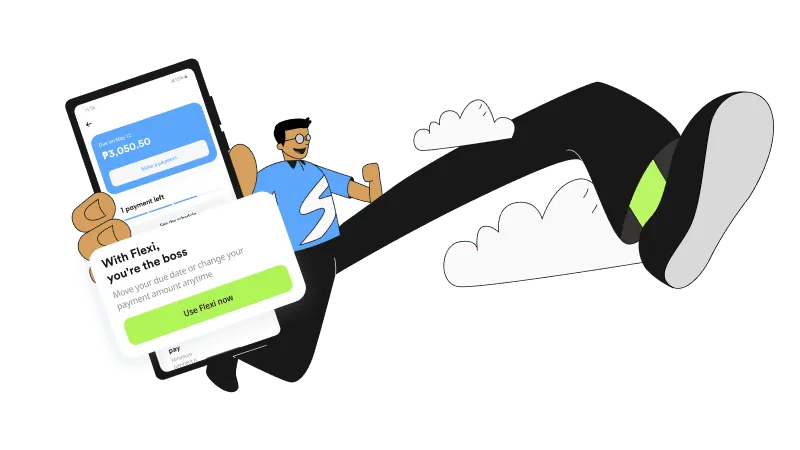

Budgeting with the 50/30/20 rule can help you stay in control of your finances, but there may be times when you need a little more flexibility. The reality is, life doesn’t always go as planned. There may be months when your budget feels a little tighter than usual. Some months may bring a delayed payday, unexpected expenses, or additional family responsibilities.

If you need more flexibility, Skyro offers an add-on called Flexi for their product loans and cash loans. For a small fee, you can change your payment amount and due date anytime directly through the Skyro app. Learn more about Flexi here.

Did this help?

See all articles

4.7

46.7K reviews on Google Play

Get approved, track your loan, and pay.